If you are trying to stay compliant with company tax in Dubai, the most important concept to get right is “taxable income”. Many businesses assume it simply means “revenue” or “profit on the P&L”, but UAE Corporate Tax uses a more specific definition: taxable income generally starts with your accounting profit, then applies a set of adjustments under the Corporate Tax law.

This guide breaks down what typically counts as taxable income, what may be excluded, and the practical steps to compute it accurately for UAE Corporate Tax returns.

Quick refresher: what “company tax in Dubai” applies to

The UAE introduced Federal Corporate Tax (CT) under Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses (as amended). The tax is federal, so the same framework applies across Dubai and other Emirates.

In practice, most businesses will come across these baseline rules:

- Corporate Tax is generally 0% on taxable income up to AED 375,000, and 9% on taxable income above AED 375,000 (subject to the specific rules that apply to your entity).

- Returns and payments are generally due within 9 months after the end of the tax period. (For planning, see ADS Auditors’ guide on corporate tax return deadlines.)

- Free zone entities may be eligible for a 0% rate on certain income if they qualify as a Qualifying Free Zone Person and meet the relevant conditions.

For official references and updates, it is worth reviewing the UAE Ministry of Finance Corporate Tax hub and guidance, starting with the UAE Ministry of Finance Corporate Tax page.

For detailed timelines, read: Corporate Tax Return Deadlines in UAE

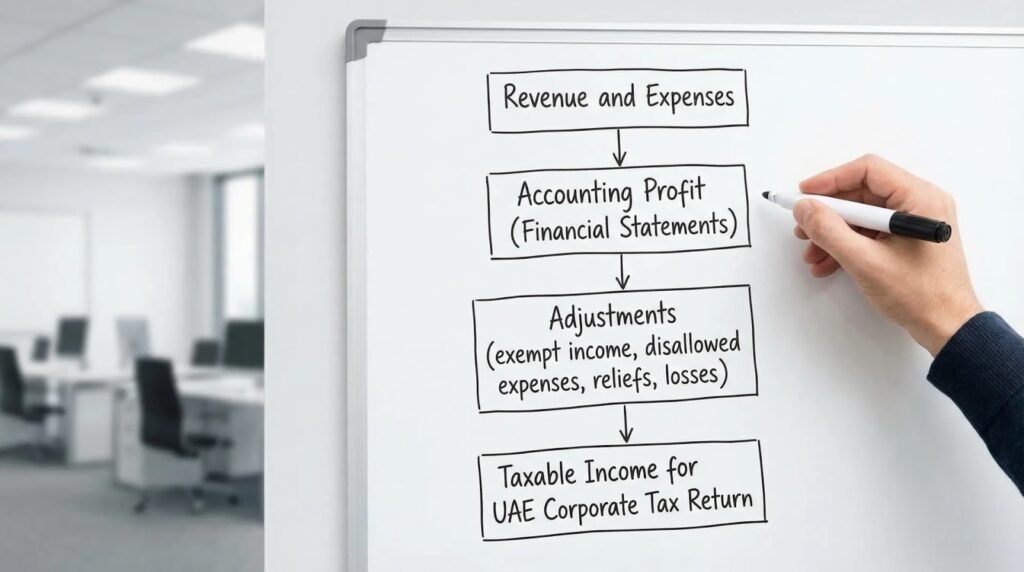

What is taxable income in UAE Corporate Tax?

Taxable income is not the same as revenue. In most cases, UAE Corporate Tax uses your business’s accounting results as a starting point, then applies specific tax adjustments.

A practical way to think about it:

Taxable income = Accounting profit (or loss) for the period, adjusted for items the Corporate Tax law treats differently.

Those adjustments are where most errors happen, and where professional review often saves money and reduces audit risk.

The typical starting point: your financial statements

For many businesses, the starting point is the accounting profit shown in IFRS-based financial statements (or other acceptable standards in specific cases). If your bookkeeping is weak, taxable income calculations become guesswork, and that usually leads to either overpaying tax or filing an exposed position.

If you want a practical benchmark for what “good” looks like for SMEs, ADS Auditors’ post on accounting advisory deliverables for UAE SMEs is a useful reference.

What counts as taxable income

Most operating income is taxable unless a specific exemption or special regime applies.

Here is a high-level view of common income types and how they are usually treated under UAE Corporate Tax. Exact treatment can depend on facts, elections, and documentation.

| Income type (examples) | Usually taxable? | Notes (what to check) |

| Sales of goods (trading revenue) | Yes | Recognized under your accounting policy, then adjusted if tax rules require it. |

| Service income (consulting, contracting, retainers) | Yes | Watch revenue recognition and cut-off at year-end. |

| Subscription or SaaS-type recurring income | Yes | Ensure deferred revenue is handled consistently. |

| Rental income (commercial leasing, equipment leasing) | Generally yes | Classification and related expenses matter. |

| Interest income (bank interest, related-party loans) | Generally yes | Related-party pricing and documentation may apply. |

| Royalties and IP income | Generally yes | Cross-border payments may trigger additional considerations beyond CT. |

| Foreign exchange gains | Often yes | Treatment can vary by whether gains are realized or unrealized, and your accounting approach. |

| Dividends received | Sometimes exempt | May qualify for participation exemption if conditions are met. |

| Capital gains on shares | Sometimes exempt | May qualify for participation exemption if conditions are met. |

| “Other income” (insurance claims, recoveries, grants) | Depends | You need to review the nature of the receipt and related expenses. |

| Intra-group management fees | Generally taxable for recipient | Also a transfer pricing and substantiation issue. |

Key takeaway

If the income increases your accounting profit, assume it is taxable unless you can support a clear exemption or special rule.

Income that may be excluded from taxable income (common exemptions)

UAE Corporate Tax includes exemptions that can remove certain income from taxable income, provided you meet the conditions and keep evidence.

Two common areas businesses ask about:

1) Dividends and gains from investments (participation exemption)

In many jurisdictions, corporate tax systems exempt certain dividends and capital gains to avoid double taxation. The UAE Corporate Tax system includes concepts along these lines, but the exemption is not automatic for every dividend or share sale.

What to verify with your tax advisor:

- Does your shareholding meet the required conditions for exemption?

- Is the income properly recorded and supported (board resolutions, dividend vouchers, sale agreements, valuation support, etc.)?

- Are there any anti-abuse or minimum ownership/holding requirements that apply to your fact pattern?

2) Foreign operations (and avoiding double taxation)

If your business has foreign branches, permanent establishments, or overseas income streams, there may be mechanisms to avoid double taxation, but they are technical. This is where the “taxable income” story often becomes an “international tax” story.

If this applies to you, see ADS Auditors’ overview of international tax basics for SMEs and consider structuring advice early.

Adjustments that change your taxable income

Most Corporate Tax computations in the UAE are a series of adjustments to accounting profit. The biggest categories are:

Disallowed or limited deductions (expenses that do not fully reduce taxable income)

A business can be profitable on paper but still have a higher taxable income if some expenses are not deductible.

Common examples businesses should review:

- Fines and penalties: Many tax systems restrict deductibility of government penalties.

- Entertainment and certain client hospitality: Deductibility may be limited (often a partial disallowance) depending on the rules and the nature of spend.

- Donations, gifts, and sponsorships: Treatment depends on who the recipient is and whether it is considered wholly and exclusively for business.

- Owner or related-party expenses booked through the company: These are a frequent adjustment area in SMEs.

The lesson is simple: if an expense is not strictly business-related, it is likely to be challenged and may increase taxable income.

Interest and financing costs (often subject to limitation rules)

Debt is common in UAE businesses, especially in real estate, trading, and group structures. Interest and financing costs may be subject to limitation rules, which can increase taxable income even if your P&L shows a lower profit.

Practical implication: a company can be cash-stressed and still have taxable income that is higher than expected.

If cash flow is a concern, planning ahead matters. ADS Auditors’ post on whether corporate tax can be paid in installments can help you think through options.

Related-party transactions and transfer pricing

If you transact with owners, sister companies, parent entities, or overseas affiliates, taxable income may change due to:

- Transfer pricing adjustments (arm’s length principle)

- Documentation expectations (especially where values are material)

- Substance and commercial rationale

Even if the numbers are “right”, lack of documentation can turn a reasonable position into a high-risk filing.

Free zone companies: what counts as taxable income depends on the regime

A common misconception is: “Free zone means no corporate tax.” Under the UAE Corporate Tax framework, it is more nuanced.

If a free zone entity qualifies as a Qualifying Free Zone Person, it may benefit from a 0% rate on qualifying income, while other income may be taxed at the standard rate.

Because the boundary between qualifying and non-qualifying income is fact-specific, it is best to treat free zone tax as a classification exercise supported by:

- Proper financial statements (often audited, depending on the rules that apply)

- Clear revenue segmentation

- Substance evidence

- Correct contract and invoicing flows

If your business operates across free zone and mainland customers, or uses multiple entities, get the model reviewed early. Errors here can change taxable income significantly.

Tax losses: when low profit can still matter

Taxable income is calculated per tax period, but businesses do not always grow in a straight line. The UAE CT system includes loss relief concepts that may allow losses to be carried forward (and in some structures, relieved within a group), subject to conditions.

Common areas to check:

- Whether tax losses are available based on your taxable income calculation (not just accounting loss)

- Ownership continuity and business continuity conditions

- Whether group relief or tax group options apply

This is one of the most valuable areas for professional support because it can reduce taxable income in future periods, but only if handled correctly and consistently.

A simple example: from accounting profit to taxable income

Assume a Dubai mainland LLC has the following for the year:

- Revenue: AED 2,500,000

- Expenses: AED 2,050,000

- Accounting profit: AED 450,000

Now assume within expenses there is:

- AED 40,000 in non-deductible items (for example, penalties and non-business costs)

- AED 30,000 entertainment spend where only 50% is deductible (illustrative, confirm your facts and rule applicability)

And within income there is:

- AED 60,000 dividend income that qualifies for exemption (subject to conditions)

A simplified taxable income computation might look like:

| Item | Amount (AED) |

| Accounting profit | 450,000 |

| Add back non-deductible expenses | +40,000 |

| Add back disallowed portion of entertainment (50% of 30,000) | +15,000 |

| Subtract exempt dividend income | -60,000 |

| Taxable income | 445,000 |

Now apply the headline rates (simplified view):

- First AED 375,000 at 0%

- Remaining AED 70,000 at 9%

- Corporate Tax (illustrative): AED 6,300

The point is not the exact tax amount, it is the mechanics: taxable income moves based on adjustments, not just revenue.

Documentation that supports taxable income

When the FTA reviews a Corporate Tax return, it typically cares about the story behind the numbers. Strong documentation makes your taxable income position defensible.

At a minimum, most businesses should be able to produce:

- Trial balance and general ledger

- Bank statements and reconciliations

- Sales invoices, contracts, and revenue recognition support

- Expense invoices and approval trail

- Related-party agreements (and pricing support)

- Fixed asset register and depreciation workings

If you want a broader view of compliance discipline (and why it impacts financing and reputation), ADS Auditors’ article on why tax compliance drives growth and credibility is a helpful read.

Common taxable income errors businesses make in Dubai

Even well-run SMEs fall into a few repeat traps:

- Treating revenue as taxable income (and missing adjustments that would reduce tax legally)

- Mixing VAT logic with Corporate Tax logic (VAT is transaction-based, CT is profit-based)

- Under-documenting related-party charges (fees that look like profit shifting get attention)

- Assuming free zone income is automatically 0% without qualifying analysis

- Leaving tax work until the deadline and then filing based on incomplete books

If you are building your internal process, pair this topic with ADS Auditors’ guide to UAE corporate tax filing procedures so the calculation and filing workflow stay aligned.

Frequently Asked Questions

Is taxable income the same as accounting profit?

Not always. Taxable income generally starts with accounting profit, then adjusts for exempt income, non-deductible expenses, losses, and other tax rules.

Do I pay company tax in Dubai on revenue or profit?

Corporate Tax is applied to taxable income, which is closer to profit than revenue, but it can differ from P&L profit due to tax adjustments.

Are dividends taxable under UAE corporate tax?

Some dividends may be exempt if conditions are met (often linked to participation exemption rules). You should confirm eligibility and keep supporting documents.

Are free zone companies exempt from corporate tax?

Not automatically. A free zone entity may benefit from 0% on qualifying income if it meets the requirements to be treated as a qualifying free zone person. Other income may be taxed at the standard rate.

Can expenses always reduce taxable income?

No. Some expenses may be disallowed or only partially deductible. Common risk areas include penalties, non-business costs, and certain entertainment or hospitality spend.

What records should I keep to support taxable income?

Keep clean bookkeeping, invoices, contracts, bank reconciliations, and documentation for related-party transactions and any claimed exemptions. Strong documentation reduces penalty and audit risk.

Need help calculating taxable income for company tax in Dubai?

If you want confidence that your taxable income is calculated correctly and that you are not overpaying or taking unnecessary filing risk, consider a review by a corporate tax specialist.

ADS Auditors provides corporate tax consultancy, accounting support, and compliance guidance tailored to UAE businesses. Explore the firm at ADS Auditors and align your taxable income calculation with your filing, documentation, and planning process before deadlines close in.